Economic Update October 2023

Quarterly Market Update

The highlights:

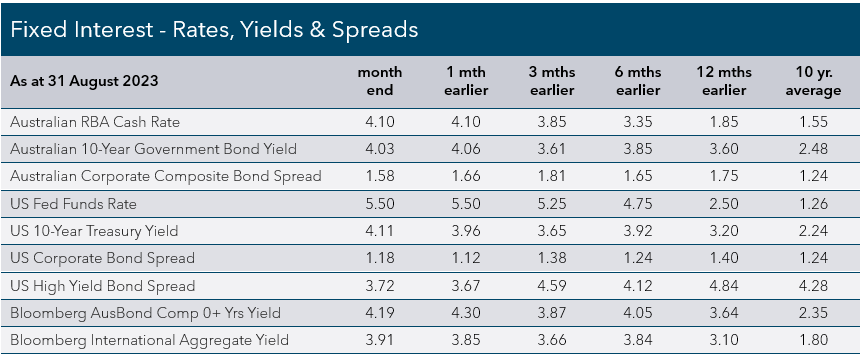

The Reserve Bank of Australia (RBA) held the cash rate at 4.1% in its September meeting heartened by softer-than-expected inflation data.

United States (US) Federal Reserve (Fed) Chair Jerome Powell struck a balanced tone in his Jackson Hole speech, repeating the Fed was “prepared to raise rates further if appropriate” while stressing the Central Bank would “proceed carefully” and be guided by economic data.

Market volatility resurfaced in August, with most asset classes initially experiencing a sharp sell-off only to regain some ground later in the month as a higher-for-longer interest rate narrative gave way to talk of a soft-landing.

August was a tough month for global shares as investors contended with higher bond yields and softer economic data from China and Europe. Fixed interest (bond) markets were mixed.

Economic Review

Australia

Inflation data for July was softer than expected. The annual headline Consumer Price Index (CPI) fell from 5.4% in June to 4.9% in July, largely driven by volatile items such as fuel, fruit and vegetables, and travel. Excluding these items, core CPI was also weaker, rising 5.8% on increasing rent and energy costs, but down from 6.1% in the previous month. The unemployment rate was steady at 3.7% in July with a small reduction in the number employed offset by a lower participation rate.

Against this backdrop, the RBA held the cash rate at 4.1% in its early September meeting with the accompanying statement a near-carbon copy of the previous month. RBA Governor Philip Lowe, delivering his final rate decision before stepping down, said while inflation is still well above its 2-3% target band (the RBA forecasts inflation getting there in mid-2025), it is now falling as the effects of higher interest rates impact household spending. The potential for further rate hikes will be data-dependent.

US

Overall, US economic data remained solid. Services Purchasing Managers’ Index (PMI) — a leading indicator of inflation — rose to a better-than-expected 54.5 (a score over 50 indicates expansion) in August, the highest reading since February. Although August brought another strong month of job gains, data pointed to slowing growth. 187,000 jobs were added versus the 170,000 expected, but significant downward revisions to the prior two months resulted in the three-month moving average trending lower. The unemployment rate unexpectedly rose from 3.5% to 3.8% and wage growth slowed, firming the likelihood of the Fed keeping the federal funds rate on hold at its September meeting.

On the inflation front, annual Personal Consumption Expenditures (PCE) — the Fed’s preferred inflation measure — rose slightly in July to 3.3%, and to 4.2% after excluding food and energy. The reaction to Fed Chairman Jerome Powell’s speech at the Jackson Hole Symposium was largely positive. Powell hit some hawkish tones, emphasising the uncertain and long road ahead for the Fed’s path on rates, but his overall stance was viewed as middle-of-the-road, reiterating the Central Bank is still watching economic data closely.

Europe

The economic outlook in Europe remains uncertain, with manufacturing and services PMI signalling a steepening downturn, hitting a 33-month low of 47.0 in August. The unemployment rate remained unchanged in July at 6.4%. Annual headline inflation was flat in August at 5.3%, while core inflation eased, also to 5.3%. Although moderating, inflation remains well above the European Central Bank’s (ECB) target and markets continue to price further rate hikes before the end of the year. The ECB meets later in September.

Headline CPI in the United Kingdom (UK) moderated in July to 6.8%, but core inflation remained unchanged at 6.9%. Concerns high inflation could become entrenched in the UK were further reinforced by strong private-sector wage growth data. While the UK economy continues to experience modest growth, PMI fell below 50 in August indicating a contraction in business activity.

Asia

Manufacturing and services activity in China expanded at its slowest pace in eight months, with composite PMI down as the reopening boost from COVID continues to fade. Weak consumer spending has meant China is grappling with fears of deation (falling prices) rather than ination, but annual headline CPI did move back into positive territory in August, rising 0.1%. In an encouraging step, Beijing announced a number of easing measures to support the fragile property sector, consumption and currency. Annualised gross domestic product (GDP) growth in Japan came in at 6.0% for the June quarter, with forward-looking indicators pointing to a continuation of strong momentum in economic activity. Annual core CPI inflation lifted from 4.2% in June to 4.3% in July.

Asset Class Review

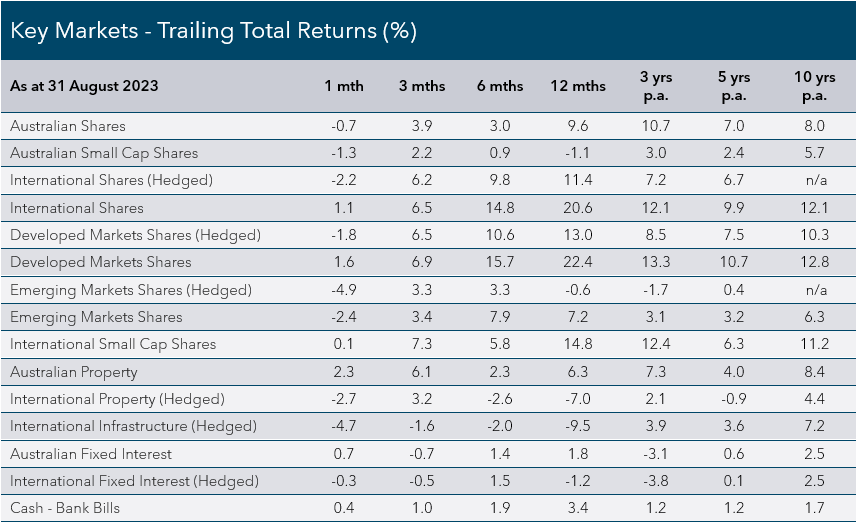

Australian Shares

After falling more than 4% in the early part of the month, the S&P/ASX 200 Index clawed most of its losses to close down -0.7% by the end of August, outperforming most other major global markets. Small companies lagged large companies — the S&P/ASX Small Ordinaries Index retracing -1.3%. The full-year reporting season took centre stage in August. While results were marginally ahead of expectations, share prices were highly volatile with one in eight companies moving more than 10% up or down, almost double the average. The key theme was the persistent pressure of rising costs (both wages and interest), which was reflected by dividends falling relative to the rise in earnings, and on balance drove downgrades to the outlook for earnings for the 2024 financial year.

Consumer discretionary (+5.7%) outperformed as results were better than the market had initially feared, while real estate (+1.6%) benefited from softer bond yields domestically. Energy (+0.5%) made gains as supply cuts collided with improved macroeconomic sentiment and strong global demand to send oil prices higher. The market ditched defensives despite falling bond yields, with consumer staples (-3.2%) and utilities (-3.8%) suffering the biggest falls. Commodity prices fell as sentiment towards the Chinese property market soured, dragging materials (-2.0%) lower.

Fund Managers Are Saying:

“This recent result season showed the last year's earnings to be generally in line with expectations. Over the past year, revenues have held up, although margins have come under some pressure. But the biggest risk we see is next year's earnings guidance. Underpinning these results are three key themes:

1. Costs: Specifically labour costs, funding costs and CAPEX (capital expenditure) costs are impacting earnings. Companies that have had higher labour costs, but cannot pass them through, have generally underperformed.

2. The consumer: As anticipated, we are seeing evidence of deteriorating consumer demand, driven by ongoing cost of living pressures, higher interest costs, the ‘mortgage cliff’ and dwindling savings buffers. This slowdown in demand is occurring at a time when businesses are seeing broad-based cost inflation.

3. China: With a disproportionate impact on commodity prices (China represents 50% of commodity demand for copper, alumina and coal), China’s slowing impacted the commodity sector. Weaker commodity prices also contributed to a lower Australian dollar making companies with offshore earnings more attractive.”

Fidelity International

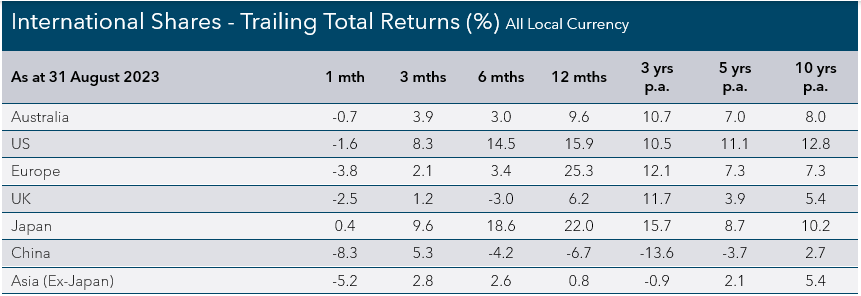

International Shares

International shares were weaker in August on higher bond yields and amid concerns about higher-for-longer interest rate expectations and slowing momentum in the Chinese economy and its fragile property sector. The MSCI All Country World Hedged Index retreated -2.2%, while unhedged shares rose +1.1%, benefiting from a sharp fall in the Australian dollar against most major currencies. Performance was negative across all developed market sectors with the exception of energy (+2.6%), which gained on higher oil prices, while healthcare (-0.2%) also held up well. Utilities (-4.8%), materials (-3.1%), financials (-2.8), and real estate (-2.5%) were the worst performers.

US shares lost ground in August as bond yields rose on the back of better-than-expected US economic data. The S&P 500 Index dropped -1.6%, while the technology-heavy Nasdaq posted its first monthly decline since February, falling -2.1%. Weaker local economic news combined with expectations of further rate increases drove European and UK shares lower, with the Euro Stoxx 50 Index down -3.8% and the FTSE 100 Index off -2.5%.

Emerging markets significantly underperformed developed markets, with the MSCI Emerging Markets Index (hedged) dropping -4.9%. Expectations of higher US interest rates — which increase the cost of borrowing in emerging markets — as well as concerns about China, contributed to a deterioration of risk sentiment in the region. Japanese shares rose in August with the Topix Total Return Index returning +0.4%, again driven by the more domestically oriented mid and small-cap company sector.

Fund Managers Are Saying:

“After a bumper start, China’s rebound since the end of its zero-Covid policy is underwhelming investors. Earnings estimates are on a downward path, youth unemployment is at record highs, and Chinese consumers haven’t resumed their zeal for spending. This does not mean China’s rebound has run its course. It is perhaps no surprise that consumer confidence is muted after three years of severe restrictions. And there are positives elsewhere, including accommodative monetary and fiscal policies and an improving regulatory backdrop. Further stimulus measures may arrive soon. Meanwhile, the disjunct between the market’s expectation and the reality of the recovery has left Chinese equities trading at a significant discount.”

Fidelity International

Property and Infrastructure

Australian listed property followed a strong July with further gains in August, buoyed by a strong performance from index heavyweight Goodman Group and the growing prospect local interest rates have peaked. The local S&P/ASX 200 A-REIT Index lifted +2.3%. Global property didn’t fare so well. The FTSE EPRA Nareit Developed Index (Hedged) — which is dominated by US-listed property — fell -2.7% as shrinking yield spreads (income differentials) compared to the 10-year Treasury and concerns surrounding commercial real estate debt have led investors to shun the sector. Rising expectations the Fed will have to keep rates higher was also a drag on global listed infrastructure, which had a difficult month with the FTSE Global Core Infrastructure 50/50 (Hedged) Index off -4.7%.

Fixed Interest

Fixed interest (bond) markets fell in early August as bond yields spiked on the higher-for-longer interest rate narrative, only for bonds to regain some of those losses late in the month as yields rose on renewed concerns about China’s property market and its broader economy. The Bloomberg Global Aggregate Bond Hedged Index fell -0.3%, but the Australian fixed interest market performed well with the Bloomberg AusBond Composite 0+ Yr Index gaining +0.7%.

Despite the intra-month volatility, Australian and US government bonds both generated positive returns in August. The 2-year Australian Government Bond yield ended 0.23% lower at 3.81%, while the 10-year Australian Government Bond yield was also down modestly to 4.03%, having been as high as 4.28% earlier in the month. The 2-year US Treasury yield was virtually unchanged at 4.85%, while the 10-year US Treasury yield rose 0.15% to 4.11%, having peaked at 4.34% and its highest level since 2007 earlier in the month.

Credit (corporate bond) markets were more mixed, with Australian investment-grade credit returning +1.0% and significantly outperforming global investment-grade which fell -1.0%. A bleaker economic outlook resulted in negative total returns and wider spreads for European investment-grade credit. US investment grade credit underperformed European investment-grade. Global high yield credit fared better, slightly outperforming government bonds. The Australian money market is predicting one further cash rate hike, with the three-month bank bill swap rate (widely used to set lending rates) ending August at 4.13%.

Fund Managers Are Saying:

“As we saw in the great inflation unwind of the 80s, the disinflation process can remain uneven, and take time. Current market sentiment is that improvement in inflation has run its course but may follow a similarly uneven process. Against this backdrop, long-term yields have surged back to their highs. Overall, tighter credit conditions, a challenged consumer, weaker global growth and inflation all reinforce decelerating inflation trends. Over time, we believe short rates will eventually be reduced, and the outlook for a broad variety of fixed-income sectors will be favourable.”

Western Asset Management

All financial services included in this communication are authorised by Infinity Financial Consultants, Infinity Financial Consultants Pty Ltd is a Corporate Authorised Representative of Infinity Advisor Australia Pty Ltd ABN 53 636 060 609 AFSL No. 519295. It is general information only and does not constitute financial product advice. If any statements made (either alone or together) constitute advice, then the advice is general advice only and does not take into account anyone’s objectives, financial situation or needs. This document is based on information considered to be reliable. It is based on our judgement at the time of issue and is subject to change. No representation, warranty or undertaking is given or made in relation to the accuracy or completeness of the information presented in this document. Except for liability that cannot be excluded, Infinity Financial Consultants, its directors, employees, agents, and related bodies corporate disclaim all liability in respect of any error or inaccuracy in, or omission from, this document and any person’s reliance on it. This material is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. If this document contains any performance data, then performance is not a reliable indicator of future performance.