Economic Update December 2023

The highlights:

A ‘soft-landing’ scenario — where inflation falls back to target without significant deterioration in economic growth or employment — is again the consensus market view. Tentative signs both economic and inflation data are cooling boosted optimism that the United States (US) Federal Reserve (Fed) is finished with its aggressive rate-hiking campaign and sparked large rallies in shares and bonds in November.

A faster-than-expected decline in the pace of inflation was not just a US story but a common theme across all major economies. Global central banks, for the most part, have hit the pause button on rate hikes, and markets have brought forward expectations around the timing of a pivot to rate cuts.

The rollercoaster ride in bond yields continued through November. Led by US Treasuries, bond yields tumbled from decade-highs to support broad-based gains in bonds, reversing the sharp sell-off in October.

Global shares soared higher on the back of falling bond yields, with all major global markets posting exceptional results in November. Australian shares followed global markets higher, with gains from small companies particularly strong.

Economic Review

Australia

The monthly Consumer Price Index (CPI) report showed a sharp drop in annual headline inflation from 5.6% to 4.9%, while core CPI retreated from 5.5% to 5.1% in October. This was more than expected, but a bias in the monthly data towards goods inflation rather than services inflation, which remains elevated, means the results were greeted with a degree of caution. The labour market added another 55,000 jobs in October, while the unemployment rate remained unchanged at 3.7%. Wages growth was 1.3% in the September quarter and 4.0% for the year. The Reserve Bank of Australia (RBA) expects wage growth to stabilise at around this annual level before declining gradually as pressure in the labour market eases, aided by an increase in net migration.

The RBA ended the year by leaving the cash rate unchanged at 4.35% at its early December meeting, where it will stay until at least February when the central bank meets again. Sticky services inflation means the RBA has left the door open to a further rate hike in 2024. The RBA reiterated any decision to hike will depend upon incoming inflation and jobs data, with the all-important December quarter CPI set to be delivered at the end of January. The RBA is projecting headline CPI will fall to 4.5% annually, down from 5.4% recorded in the September quarter. The market is pricing a rate cut in late 2024.

US

As expected, the Fed kept rates on hold at 5.25%-5.50% at its early November meeting. The October CPI report, which was released later in the month, confirmed inflation continues to trend lower. Annual headline CPI fell to 3.2% in October, down from 3.7% in September, raising hopes inflation is on course to fall back to the Fed’s 2% target without the need for further rate hikes. Core CPI remained stickier with the annual change falling from 4.1% to 4.0%.

While markets appear convinced rates have peaked and are now pricing in rate cuts starting in mid-2024, the Fed is still talking up the need to avoid complacency and said it is prepared to hold rates at elevated levels for an extended period. The Fed will also be keen to ensure that falling bond yields — based on expectation of earlier rate cut — do not undermine its efforts to slow inflation. Economic data painted a mixed picture of the economy. September quarter annualised Gross Domestic Product (GDP) was revised upward to 5.2%, but the manufacturing Purchasing Managers Index (PMI) indicated a contraction in activity.

Europe

There was also a steeper-than-expected fall in inflation in Europe, which like in the US, prompted hopes that rate cuts were near. Estimated annual inflation for November was 2.4%, down from 2.9% in October. The ECB did not meet to discuss monetary policy (interest rate settings) in November, but comments from the central bank suggested rates would need to remain at the current level of 4.50% for an extended period of time before inflation would come back to the 2% target. Composite manufacturing and services PMI for November showed business activity continuing to fall.

October annual headline CPI inflation in the United Kingdom (UK) came in at 4.6%, down sharply from the 6.7% recorded in September. The report contributed to optimism the Bank of England (BoE) has finished with its current rate hiking cycle — which has involved more than 5% worth of hikes between December 2021 and August 2023 in a bid to combat soaring inflation. There were also signs economic activity is bottoming in the UK, with November services PMI moving above the 50 market, signaling a shift from economic contraction to expansion.

Asia

Inflation in China fell at its fastest rate in three years in November, with annual headline CPI dropping -0.5%. The result highlights the daunting task faced by Chinese authorities to revive demand, particularly with the significant drag on growth the problematic housing market is creating. The People’s Bank of China injected liquidity into the banking system once again, and a new required reserve ratio cut — allowing banks to lend out more — could arrive before year-end.

Asset Class Review

Australian Shares

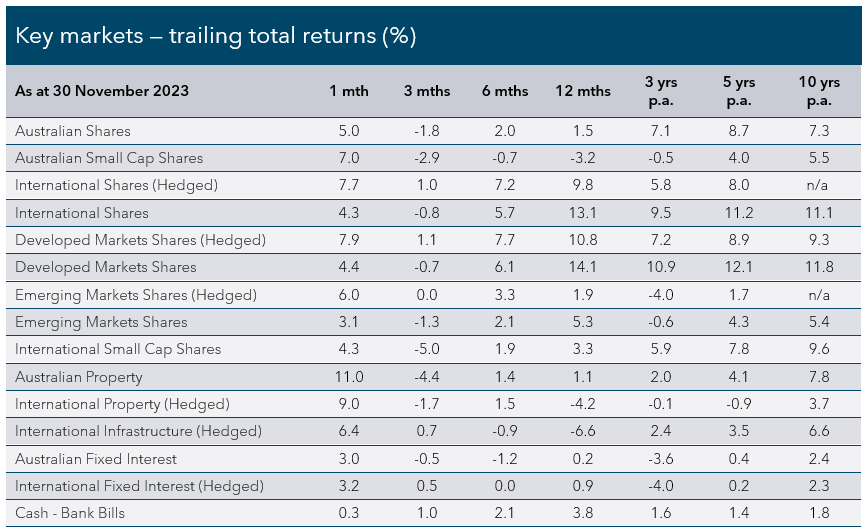

The S&P/ASX 200 Index gained +5.0% in November. Expectations of lower interest rates and risk-on sentiment were catalysts for an impressive rally in small companies that outperformed their larger peers — the S&P/ASX Small Ordinaries Index jumped +7.0%. Most sectors enjoyed significant gains over the month, with recent laggards’ healthcare (+11.7%), real estate (+10.8%), and information technology (+7.3%) the biggest winners. The worst performers were energy (-7.4%) on falling oil prices due to moderating demand and underwhelming OPEC+ supply cuts, and utilities (-6.0%).

What fund managers are saying…

While many commentators lament the increased market ‘uncertainty’ ahead that is supposedly a function of higher rates and the re-emergence of broad-based inflation, Airlie believes equity valuations and implied levels of risk and reward across the ASX at the moment finally reflect a return to normal.

While the ascent of interest rates in Australia over the last 12 months has been remarkably rapid, the absolute level at which they sit now is hardly egregious relative to the last 30 years. While ASX valuations have returned to more or less the average of their last 20 years.

From a company-specific perspective, there is a general sense that Australia is returning to a more normal operating cadence for many businesses, in Airlie’s opinion. Airlie sees 2024 as the return of ‘normal’, which for Airlie means a normal, healthy level of uncertainty. Uncertainty makes a market; it means dislocations and thus the potential for excellent investment opportunities.

Airlie Funds Management

International Shares

Expectations of modest economic growth coupled with falling interest rates are a potent combination for share markets and delivered the strongest monthly returns for some time in November. International shares soared higher on the back of the sharp retreat in bond yields, with the MSCI All Country World Hedged Index jumping +7.7%. A strong rally in the Australian dollar was a headwind for unhedged shares, but the MSCI All Country World Unhedged Index still gained a healthy +4.3%. The cooler-than-expected inflation readings boosted rate-sensitive sectors of the market such as real estate (+10.9%) and information technology (+13.3%). The consumer discretionary sector (+9.8%) was another strong performer, while energy (-0.9%) was the only sector to finish in negative territory.

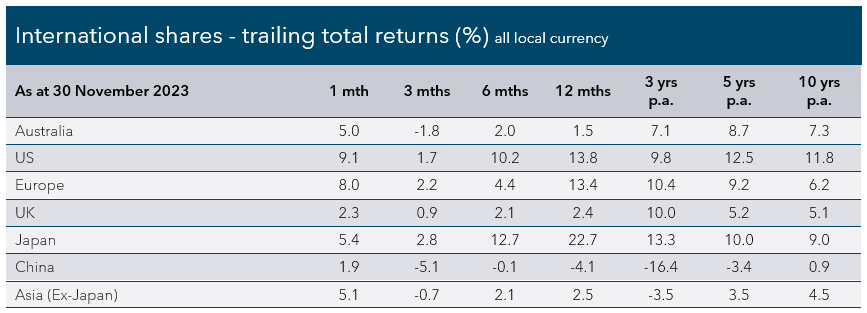

US shares ended a three-month losing streak with a spectacular recovery in November. The S&P 500 Index advanced +9.1%, and the Nasdaq jumped +10.8%, all but wiping out the 10% correction endured since recent highs were hit back in July. European shares made strong gains with the Euro Stoxx 50 Index up +8.0% as investors warmed to the idea interest rates would shortly be cut off the back of cooling inflation. The UK’s FTSE 100 Index rose +2.3% over the month but lagged other major developed markets. Emerging markets advanced, albeit not at the pace of developed markets due to the drag of the Chinese market (+1.9%) — the MSCI Emerging Markets Index (Hedged) added +6.0%.

What fund managers are saying…

We are at an interesting juncture in global equity markets. Equity markets seemed to have reached a low level in October 2022, during peak fear and pessimism. Since then, investors have increasingly gained comfort in the Fed’s ability to engineer a soft landing, and recession fears have abated. In textbook recovery fashion, valuation multiples troughed first.

The next phase of a typical recovery occurs when earnings rise and valuation multiples pass the baton to fundamentals that become the primary driver of shareholder returns. Given that we have already seen the expansion in valuation multiples, the pressure is now on for an earnings recovery to come through. Otherwise, our gains over the past 12 months might look vulnerable.

The current macroeconomic backdrop is not the most conducive to earnings recovery, with a stubborn level of inflation driving a higher-for-longer interest-rate narrative. Above-average inflation rates continue to pressure business profit margins, posing a headache for consumers stretching their household budgets.

The excess household savings accumulated throughout the pandemic lockdowns have now largely disappeared. Meanwhile, higher rates pressure the housing sector and corporate cashflows. All of this means that the explosive gains in global markets seen over the last 12 months are unlikely to be repeated next year, and there’s a good chance we’ll also see increased volatility.

Fidelity International

Property and Infrastructure

A collapse in bond yields sparked a relief rally in the interest rate-sensitive listed property sector. The local S&P/ASX 200 A-REIT Index clawed back some of the losses from previous months to post an impressive +11.0% gain in November. Global property was also stronger, with the FTSE EPRA Nareit Developed Index (Hedged) jumping +9.0%. Global listed infrastructure rebounded, with FX hedging providing a boost for the FTSE Global Core Infrastructure 50/50 (Hedged) Index, which advanced +6.4%.

Fixed Interest

Fixed interest (bond) markets had largely been pricing higher-for-longer interest rates, but softer-than-expected global inflation data drove sharp declines in bond yields and a rebound in bond prices in November. The local Bloomberg AusBond Composite 0+ Yr Index rose +3.0%, slightly underperforming global bonds, with the Bloomberg Global Aggregate Bond Hedged Index advancing +3.2%.

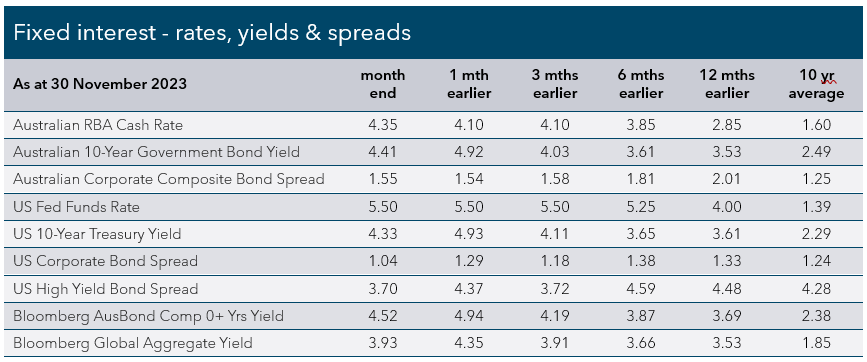

Government bond yields declined sharply. The 10-year US Treasury yield ended November at 4.33%, down significantly from the peak of 5% reached in mid-October. The 10-year Australian Government Bond yield also fell heavily, dropping 0.51% to 4.41%. At the shorter end of the curve, two-year government bond yields also saw large falls. Two-year US Treasury bond yields dropped 0.34% to 4.73%, while two-year Australian Government Bond yields retreated 0.36% to 4.11%. Given the inverse relationship between bond yields and bond prices, returns from government bonds were strong in November. The Bloomberg AusBond Treasury 0+ Yr Index rose +3.1%, while the Bloomberg US Treasury Total Return Unhedged USD Index jumped +3.5%.

Outside of government bonds, the entire fixed interest market benefited from lower yields and expectations of sooner rate cuts and an economic soft-landing — which would, in turn, mean fewer defaults from bond issuers. Investment grade credit (corporate bonds) and high-yield bonds gained as spreads tightened. Australian investment-grade credit — as measured by the Bloomberg AusBond Credit 0+ Yr Index — lifted +1.8% in November. Globally, credit performed even better, with the Bloomberg Global Aggregate Credit Total Return Index Hedged AUD and Bloomberg Global High Yield Total Return Index Hedged AUD up +4.1% and +2.7%. The Australian three-month bank bill swap rate (widely used to set lending rates) was virtually unmoved at 4.36%.

What fund managers are saying….

The persistence or lack of economic strength will dictate the timing of the Fed’s rate cutting path. But markets are forward looking. Historically, the Fed has waited too long before cutting rates. And if the Fed repeats that pattern, it then would have to cut further than if it started sooner. This is where economic fear may start to build. Our view is that the improvement in inflation trends may give the Fed the flexibility to deliver cuts without undue economic hardship. The risk case, though, remains that the Fed waits too long. In either scenario, an overweight duration is needed.

Western Asset Management

All financial services included in this communication are authorised by Infinity Financial Consultants, Infinity Financial Consultants Pty Ltd is a Corporate Authorised Representative of Infinity Advisor Australia Pty Ltd ABN 53 636 060 609 AFSL No. 519295. It is general information only and does not constitute financial product advice. If any statements made (either alone or together) constitute advice, then the advice is general advice only and does not take into account anyone’s objectives, financial situation or needs. This document is based on information considered to be reliable. It is based on our judgement at the time of issue and is subject to change. No representation, warranty or undertaking is given or made in relation to the accuracy or completeness of the information presented in this document. Except for liability that cannot be excluded, Infinity Financial Consultants, its directors, employees, agents, and related bodies corporate disclaim all liability in respect of any error or inaccuracy in, or omission from, this document and any person’s reliance on it. This material is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to local law or regulation. If this document contains any performance data, then performance is not a reliable indicator of future performance.